If you’re thinking about buying a home, you might be focusing on previously owned ones. But with so few houses for sale today, it makes sense to consider all your options, and that includes a home that’s newly built.

The Number of Newly Built Homes Is on the Rise

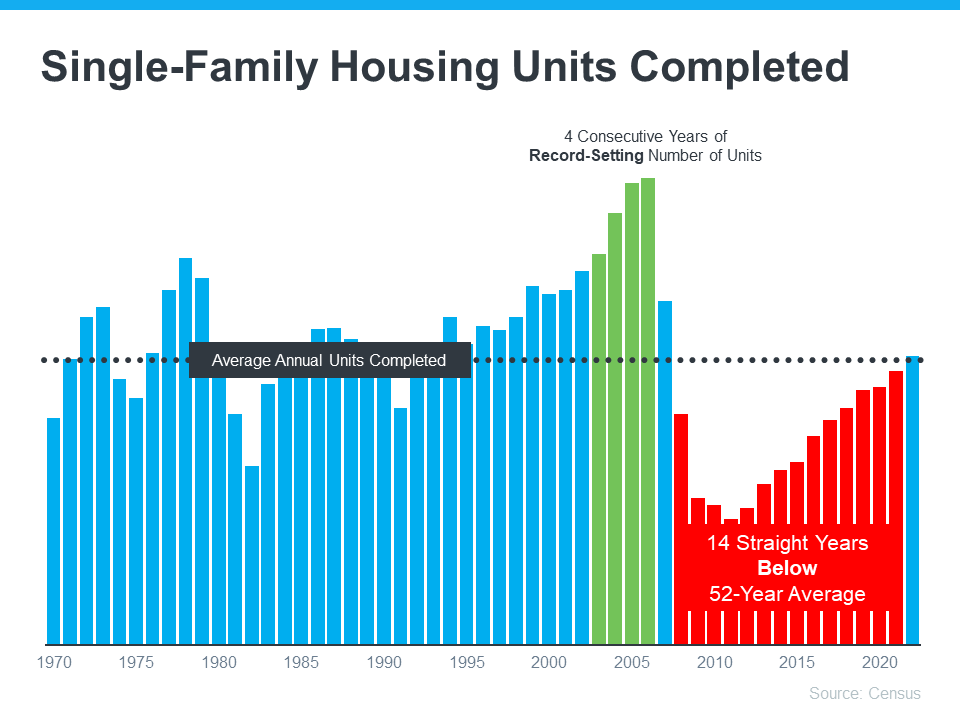

While there are more houses for sale right now than there were at this time last year, there’s still a historically low number of homes available on the market. One reason for that is years of underbuilding—meaning there haven’t been enough new homes built to keep up with demand.

The graph above shows how low the production of newly constructed homes has been over the past 14 years. But it also shows another important trend: the number of new homes being built each year is on the rise. As Mark Fleming, Chief Economist at First American, shares, that’s good news for buyers:

“While existing-home inventory remains limited, the silver lining for home buyers is that new-home inventory is on the rise, and a new home at the right price is a pretty good substitute.”

Builder Incentives Can Provide a Boost

While there a growing number of new homes for sale, builders are slowing that pace until they sell more of their current inventory. According to Logan Mohtashami, Lead Analyst at HousingWire:

“The builders have to work off the backlog of homes, but instead of 3%-4% mortgage rates, they’re dealing with 6% plus mortgage rates, which means they have to provide many incentives to make sure those homes sell.”

Many builders are now offering incentives to help buyers purchase these homes. Fleming also explains:

“The National Association of Home Builders reported that nearly two-thirds of builders were offering incentives, including mortgage rate buydowns, paying points for buyers and price reductions, which could entice potential home buyers.”

A builder who’s willing to pay to reduce your mortgage rate could be a game changer. Ksenia Potapov, Economist at First American, puts it this way:

“A one percentage-point decline in mortgage rates has the same impact on affordability as an 11 percent decline in house prices.”

Should You Buy a Brand-New Home?

The best way to decide what type of home to buy is to work with a trusted real estate professional who can help you weigh the pros and cons of each option. They know which homes are available in your local market, and which builders might be offering incentives that make sense for you.

Bottom Line

Even though there aren’t a lot of homes for sale today, new home inventory is on the rise, and many builders are offering incentives. Let’s connect so I can help you weigh the pros and cons of shopping for a new home versus an existing one.

How To Make Your Dream of Homeownership a Reality

According to a recent Harris Poll survey, 8 in 10 Americans say buying a home is a priority, and 28 million Americans actually plan to buy within the next 12 months. Homeownership provides many financial and nonfinancial benefits, so that interest is understandable.

However, it’s unlikely all 28 million Americans will accomplish that goal in the coming year. Experts project a total of around five million homes will be sold in 2023. Why is there such a big difference? It’s partly because there can be challenges to buying a home.

In the same survey, when asked, “Which of the following are preventing you from pursuing homeownership at this time?”:

- 34% answered, “I don’t have enough saved for a down payment”

- 30% answered, “My credit score”

If you’re aiming to buy a home, here’s what you need to know to accomplish that goal.

Save for Your Down Payment

Your down payment is a big chunk of what you pay up front for your home. For most home purchases, buyers put down some amount of cash up front (a down payment) and then take out a loan (a mortgage) to pay for the rest.

It’s a longstanding myth that you need to pay 20% of the purchase price for your down payment. In reality, 20% down isn’t always required. In fact, according to the National Association of Realtors (NAR), today’s median down payment is 14% for the average buyer and just 6% for a first-time buyer.

Regardless of how much money you can save for your down payment, know there’s help available. A local lender can show you options to help you get closer to your down payment goal. Plus, there are even loan types, like FHA loans, with down payments as low as 3.5% for some buyers, as well as options like VA loans and USDA loanswith no down payment requirements for qualified applicants.

Beyond assistance programs and different loan types, here are a few other tips to help you as you save for your down payment:

- Remember to factor in closing costs. In addition to your down payment, closing costs are usually 2-5% of the home's purchase price.

- Maintain your savings. Your down payment shouldn’t deplete all your savings. It’s important to still have some money set aside for homeownership expenses after you move in.

- Explore your options and lean on your trusted advisor for expert guidance. Do your research, ask questions, and look into the resources available for buyers like you.

Improve Your Credit Score

Your credit score is a number that indicates how financially reliable you are to lenders. A higher credit score usually means you’ll be able to borrow more money at a better interest rate. If your credit score is preventing you from getting an affordable mortgage, there are steps you can take to improve it. Here are two:

- Pay your bills on time. When you pay your bills on time, your credit score improves. When you’re late, it takes a hit. One way to make paying your bills on time easier? Set up automatic payments when and where you can.

- Mix it up. From auto loans, to credit cards, to mortgages – there are several different types of credit. And having a mix of them improves your credit score.

Bottom Line

If you want to purchase a home this year, let’s connect so we can start preparing.